The Math Behind Fixed vs. Variable — Simplified

Imagine your mortgage is like choosing between two kinds of phone plans — one with a fixed monthly price (no surprises) and one that changes based on usage (could be cheaper or more expensive depending on the month).

When you choose a fixed-rate mortgage, your interest rate and monthly payment stay the same for the entire term. It’s like locking in a steady phone bill — predictable and easy to plan around. A variable-rate mortgage, on the other hand, moves with the market. When rates drop, your payment can shrink and save you money; when rates rise, it can climb. Both options work, but they serve different personalities — fixed appeals to those who value stability, while variable attracts those willing to take calculated risks for potential savings.

Let’s look at the math behind it

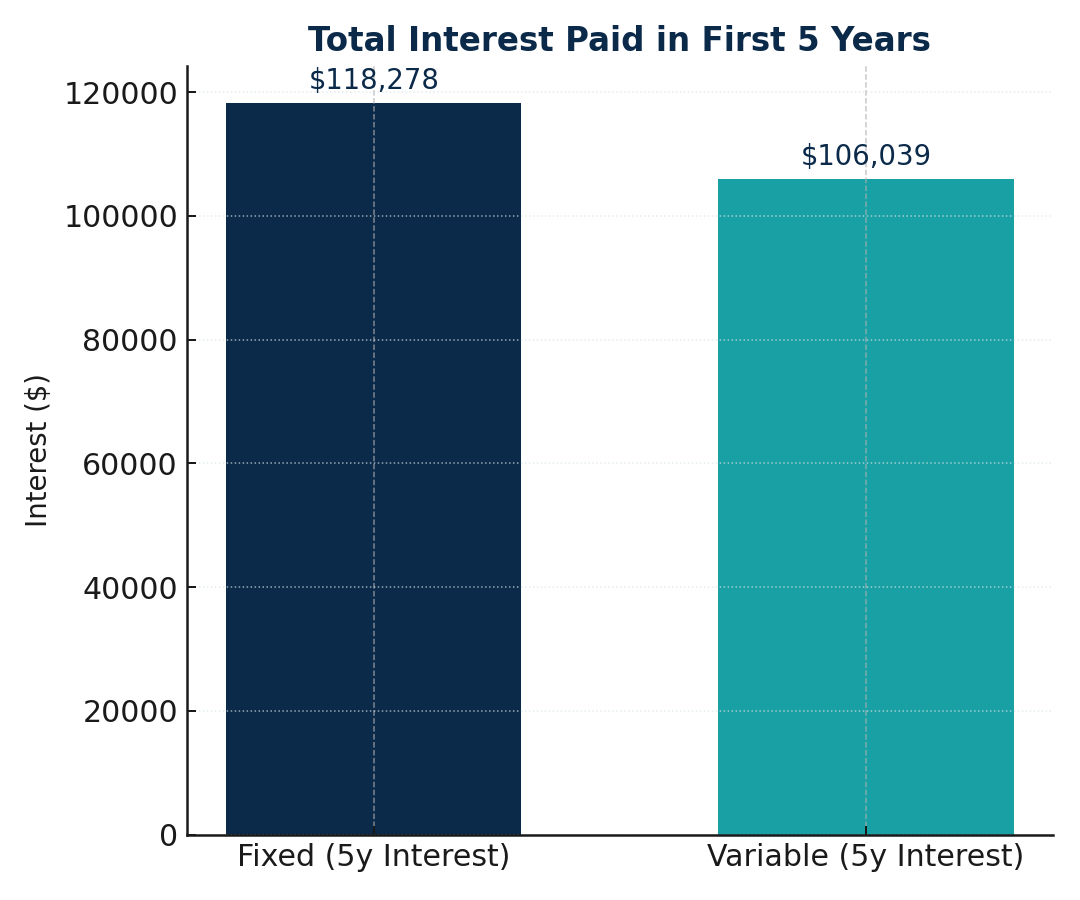

Using a $500,000 mortgage over 25 years, here’s how fixed and variable rates compare in real numbers and visuals.

| Type | Rate | Amortization | Monthly Payment | 5-Year Interest |

|---|---|---|---|---|

| Fixed | 5.00% | 25 yrs | $2,923 | $118,278 |

| Variable | 4.50% | 25 yrs | $2,779 | $106,039 |

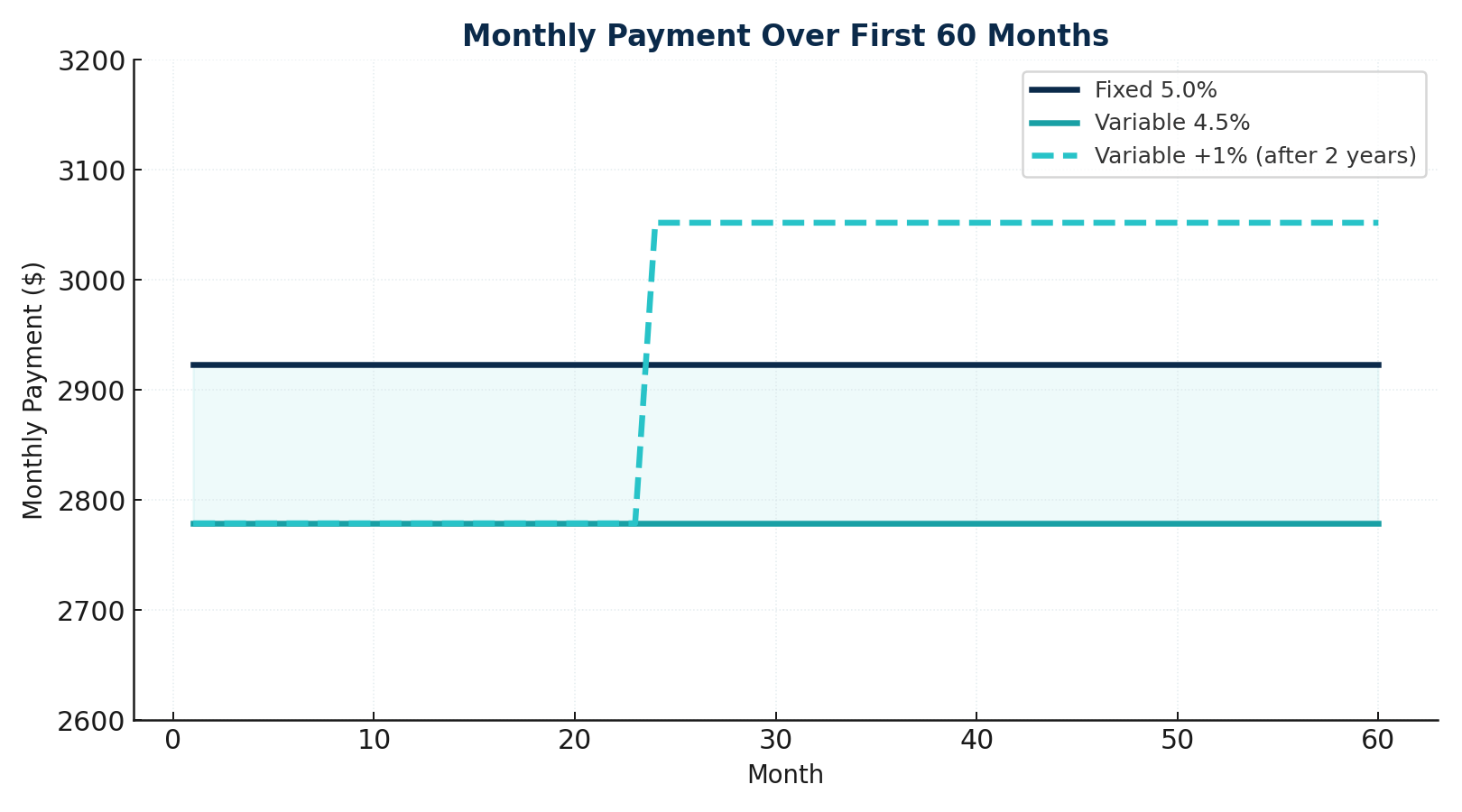

Variable starts cheaper (≈ $144/month less) — but can rise if rates climb.

At +1% rate increase (around month 24) variable payments ≈ $3,052 — same as fixed.

| New Rate | New Payment | Change vs Fixed |

|---|---|---|

| 5.50% | $3,052 | +$129 |

| 6.00% | $3,194 | +$271 |

| 6.50% | $3,339 | +$416 |

Each +1% rate ≈ +$125 to $150 per month on a $500k mortgage.